Credit: Burt Wallace TikTok video

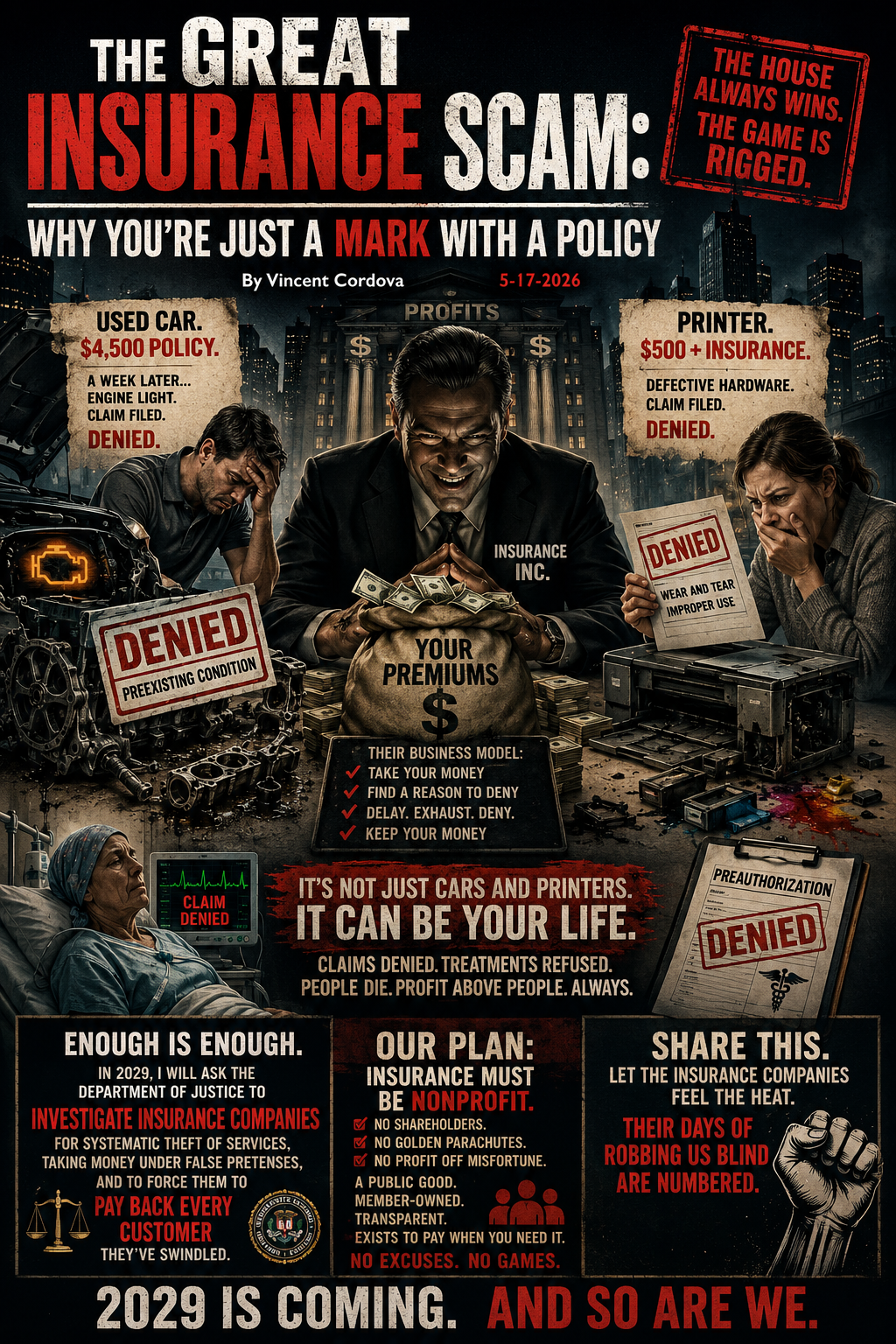

The Great Insurance Scam: Why You're Just a Mark With a Policy

By Vincent Cordova · May 17, 2026

For-profit insurance is not failing by accident. It is often behaving exactly as designed: collect first, deny later, and make the burden of fighting back heavier than the claim itself.

I just watched a video that made my blood boil. A man bought a used car. Nothing flashy, just something to get from A to B. He did what they tell you to do: he bought peace of mind. He paid $4,500 for an aftermarket insurance policy to cover mechanical failures. A week after buying the car, the engine light came on. He filed a claim. Simple, right?

Wrong.

The insurance company made the repair shop tear the entire engine apart. Days of labor. Hours of inspection. Then came the verdict: denied. The reason? A preexisting condition. A week-old problem, on a car he had owned for seven days, was suddenly something that existed before he even signed the papers. They gutted his engine and his wallet, then walked away clean.

I sat there nodding because I have been there too. A few years back, I bought a $500 printer. The store pitched me an insurance plan. Covers everything, they said. Accidental damage, mechanical failure, the whole script. I figured why not. When that printer died a few months later from defective hardware, I made the claim and got the same answer so many people get: denied. Some fine-print loophole about wear and tear or improper use. I had used it exactly as intended. It did not matter. They already had my money, and that was the point.

That is the ugly truth behind for-profit insurance. These companies are not built to help you when you need them most. They are built to collect premiums, bury the exclusions, drag out the process, and keep as much of your money as possible. Every denied claim is a financial win for them. Every exhausted customer who gives up is part of the business model.

Aftermarket insurance is one of the clearest examples because the trap is so obvious once you have lived it. They sell fear relief up front and weaponize ambiguity on the back end. They demand invasive teardowns. They stall. They force you to keep paying diagnostics, labor, rentals, missed work, and stress while they search for one phrase in the contract that lets them say no. They are betting that by the time the letter arrives, you will be too broke or too drained to fight.

But this rot does not stop at cars or electronics. It reaches into healthcare, where the stakes are not inconvenience but survival. Treatments get delayed. Prior authorizations sit in limbo. Families spend precious time arguing with a company that has already decided your emergency is a cost center. People die waiting on approvals that should never have been necessary in the first place. The same cold logic behind a denied engine claim shows up when a patient is told that life-saving care is somehow not medically necessary.

So let me be plain about where I stand. In 2029, I am going to ask the Department of Justice to investigate all insurance companies operating in this country for systematic theft of services, deceptive sales practices, bad-faith denials, and taking money under false pretenses. We are going to follow the pattern, not the press release. We are going to look at claims data, denial rates, arbitration traps, forced teardowns, delay tactics, policy language, and every mechanism designed to turn desperation into profit.

And if those investigations confirm what millions of people already know in their bones, then the response cannot be another wrist-slap fine that disappears into a government account while the executives move on. We will push for repayment. Real money back to the people who were sold coverage and handed excuses. If you took premiums for protection you never intended to provide, you should pay back the people you robbed.

This administration will also seek legislation to make insurance nonprofit. Period. If an insurance company cannot function without denying legitimate claims, then it does not deserve to exist in its current form. Insurance should be a mutual safety net. It should be transparent, member-accountable, and governed by one simple rule: when the covered loss happens, it pays. No games. No maze. No profit motive feeding on somebody else's worst day.

We have been told for decades that the free market will discipline insurers. It has not. It cannot. The profit motive does not reform claim denial. It rewards it. That is why this is not just a consumer-protection issue. It is a structural issue. The system is doing what it was designed to do, and what it was designed to do is extract.

We can build something better. Insurance can be a public good or a mutual good. It can be boring in the best possible way: clear terms, plain-language obligations, transparent oversight, automatic audit trails, and binding consequences when coverage is withheld in bad faith. People should not have to enter a psychological war zone every time they file a claim. They should be able to trust that the system exists for them, not against them.

Share this everywhere. Insurance companies have spent decades hiding behind paperwork, jargon, and exhaustion. They count on the public suffering alone. Let them feel what happens when people compare notes, connect the dots, and start demanding accountability together.

2029 is coming. And so are we.

What changes under this plan

- Launch a DOJ-wide investigation into all insurance companies and their denial practices.

- Force repayment to customers where insurers sold coverage under false pretenses or denied valid claims in bad faith.

- Work with Congress to transition insurance into nonprofit, member-serving structures.